Choosing between different types of investments can feel like navigating a vast sea without a compass, especially for those new to the world of finance. Certificates of deposit (CDs) and bonds are both popular investment options, often characterized as low-risk investments. But which one might be better suited for your financial goals? Let’s delve into this journey, comparing CDs and bonds, demystifying their benefits, and explaining how each works in detail.

Diversification is indeed the cornerstone of any robust investment portfolio. Keen on adding some crypto to your financial mix? Changelly is your go-to solution. Offering minimal fees and speedy transactions, it’s the ultimate gateway to the world of cryptocurrencies. Embark on your crypto investment journey today with Changelly!

Understanding Certificates of Deposit (CDs): What are CDs?

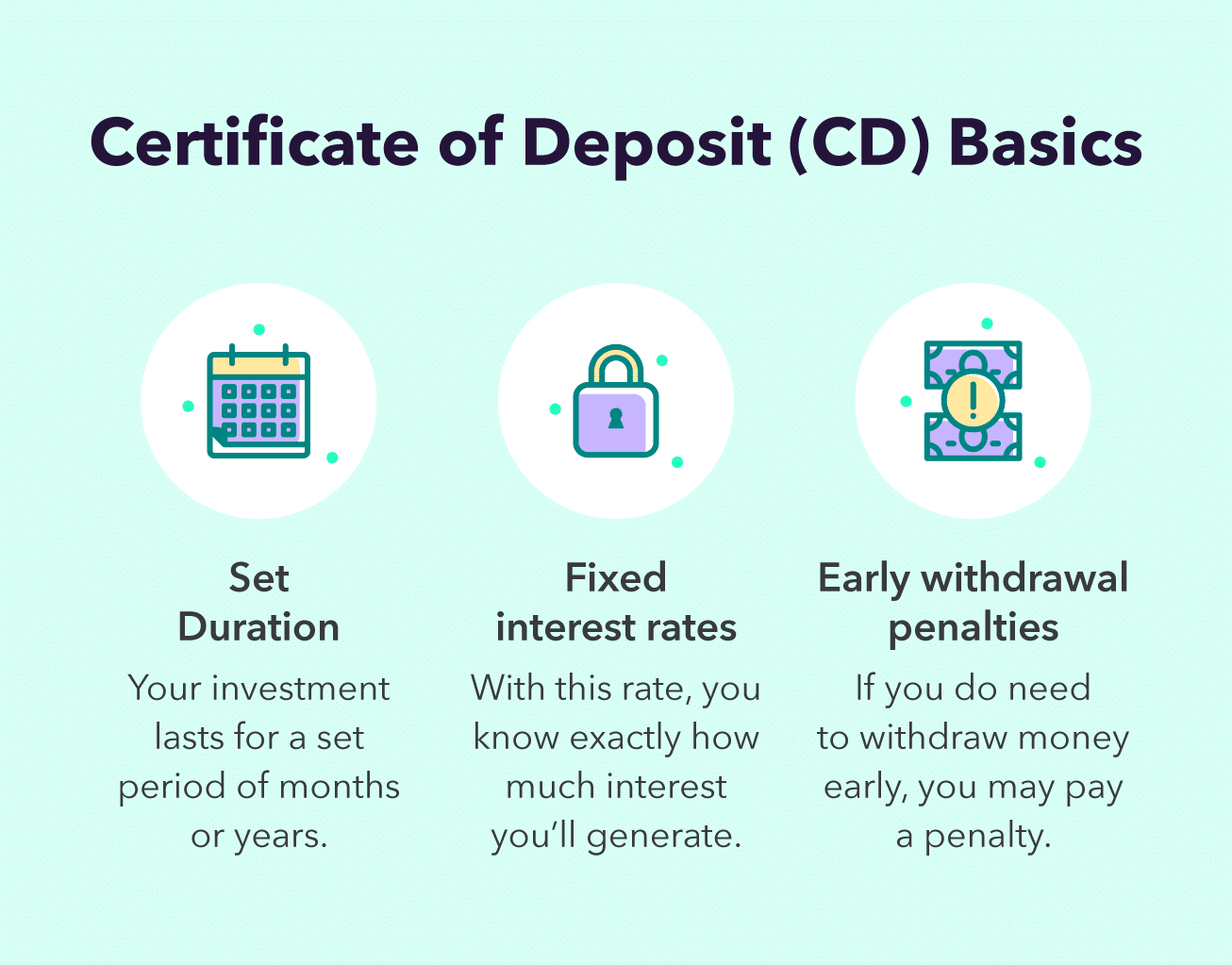

A Certificate of Deposit, or CD, is a type of savings account offered by banks and credit unions.

Unlike regular savings accounts, a CD holds a fixed amount of money for a fixed period. The period, often referred to as the “term,” can vary from a few months to several years. In return for agreeing to leave your money untouched for this term, the financial institution will pay you interest. However, there is a catch — if you need to withdraw your funds before the term ends, you’ll face an early withdrawal penalty.

Types of CDs

The world of CDs is quite diverse, with several types available:

Traditional CDs: This is the standard type of CD that most people are familiar with. You deposit your money for a fixed term and earn interest at a fixed rate. When the term ends, you get back your initial deposit plus the accumulated interest. If you withdraw your funds early, you’ll typically incur an early withdrawal penalty.

Bump-Up CDs: These offer you the chance to raise your interest rate during the term if the rates in the wider market increase. It’s a way to hedge against potential rises in interest rates. Nonetheless, the initial rate is usually lower than the rate offered on traditional CDs.

Liquid CDs: These are more flexible than traditional CDs because they allow you to withdraw part of your deposit without paying an early withdrawal penalty. That said, their interest rates are generally lower, and there may be specific rules about when and how much you can withdraw.

Zero-Coupon CDs: These types of CDs don’t pay out interest annually or semi-annually like traditional CDs. Instead, they automatically reinvest the interest earned, which means you receive a lump sum payment (original deposit plus interest) at the end of the term.

Callable CDs: These CDs can be ‘called’ or redeemed by the issuing bank before the term ends, typically when interest rates fall. This means you may not get the full interest if the bank decides to call the CD.

Brokered CDs: Brokered CDs are bought via a brokerage firm, rather than straight from a bank. Despite being initiated by banks, their selling is outsourced to firms, sparking competition and generally higher yields than traditional CDs. Brokered CDs offer more flexibility, though this can increase the potential for investment mistakes.

In the debate of CDs vs bonds, it’s worth noting that CDs, apart from offering a fixed interest rate guaranteed by the bank, are insured by the FDIC, whereas bonds can offer potentially higher yields but carry varying degrees of risk based on the issuer.

How Safe Are CDs?

CDs are widely regarded as one of the safest investment options available. Issued by banks or credit unions, they’re insured up to $250,000 per depositor by the Federal Deposit Insurance Corporation (FDIC) or the National Credit Union Administration (NCUA). This means that even in the event of the financial institution failing, you won’t lose your deposit.

When Is a CD Your Best Option?

From a professional standpoint, there are specific situations where investing in a Certificate of Deposit (CD) can be highly beneficial:

- For Defined Short-Term Goals: If you’re aiming for a specific financial target in the near future—be it a down payment on a house, purchasing a new vehicle, or embarking on a vacation of a lifetime—and you’ve already set aside the necessary funds, opting for a CD could be a wise decision. The fixed interest rate of a CD ensures the growth of your savings in a risk-free manner, shielded from any market volatility. Just make sure the term of the CD aligns with your savings timeline to circumvent any penalties for early withdrawal.

- Seeking Stability and Security: If what you value most is the assurance of stable returns and the highest level of security for your savings, then a CD stands out as a solid choice. The return rates are clear from the outset, immune to the unpredictability of market forces. Additionally, with FDIC or NCUA insurance, your investment is protected up to $250,000, offering peace of mind in the unlikely event of a financial institution’s failure.

Where Can I Open a CD?

CDs can be opened at any bank or credit union, and you can also buy them through a brokerage firm.

Delving Into Bonds: What are Bonds?

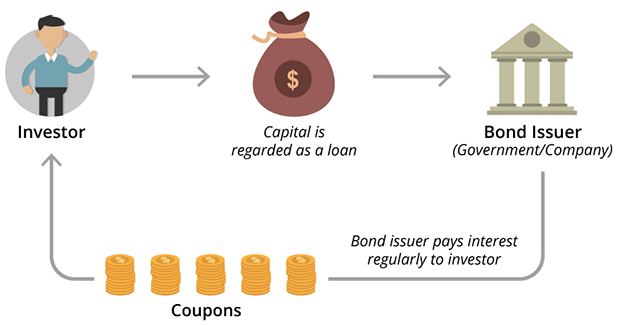

A bond is a form of loan that investors make to bond issuers, which can be corporations, municipalities, or the federal government. In return for the loan, the issuer promises to pay back the loan amount, referred to as the “principal,” by a specific date known as the maturity date. Meanwhile, the issuer also makes periodic interest payments to the bondholder.

If you’re comparing a CD vs a treasury bond, consider that treasury bonds may be a better option if you’re looking for a longer-term, lower-risk investment backed by the U.S. government.

Types of Bonds

There are several types of bonds to choose from:

Government Bonds: These are issued by the federal government and are often considered the safest type of bond. They come in three varieties: Treasury Bills (T-Bills), Treasury Notes (T-Notes), and Treasury Bonds (T-Bonds). T-Bills have the shortest maturity (up to 1 year), while T-Notes and T-Bonds have longer maturities. The interest earned on these bonds is exempt from state and local taxes.

Municipal Bonds: Issued by states, cities, or other local government entities, municipal bonds fund public projects like schools, highways, and bridges. The interest paid on these bonds is typically exempt from federal income tax and often from state and local taxes as well if you live in the state where the bond is issued.

Corporate Bonds: Companies issue corporate bonds to raise capital for a variety of reasons, from operational expansion to funding research. These bonds usually offer higher interest rates than government and municipal bonds due to their increased risk level. The safety of the bond depends on the financial health of the company.

Savings Bonds: These are non-marketable securities issued by the U.S. Department of the Treasury and meant for general public investment. They’re sold in small denominations and have long-term maturities. The most common types are Series EE and Series I savings bonds.

Agency Bonds: These bonds are issued by government-sponsored enterprises (GSEs) and federal agencies. They’re considered slightly riskier than Treasury bonds but safer than corporate bonds.

Foreign Bonds: These are bonds issued by a foreign government or a corporation located outside of your home country. Investing in foreign bonds introduces extra risks, such as currency risk, but they can offer higher returns and additional diversification.

Bond Mutual Funds: These are funds that invest in various types of bonds. Bond mutual funds offer diversification and professional management, but the returns and principal value can fluctuate.

How Safe Are Bonds?

While bonds are generally considered safe investments, their safety can vary. For instance, corporate bonds carry a risk of default, meaning the company might not be able to make interest payments or return the principal. On the other hand, municipal bonds and savings bonds are backed by government entities and are generally considered very low risk.

When Is a Bond Your Best Option?

When Is a Bond Your Best Option?

From my experience, here are key situations when bonds might be an optimal choice for your investment strategy:

- Diversifying a Stock-Heavy Portfolio: For those looking to mitigate risk within a portfolio that’s heavily weighted towards stocks, bonds can provide an effective balance. Their relatively stable nature can safeguard against the volatility often seen in stock markets, offering a smoother investment journey and enhancing overall portfolio stability.

- Seeking Steady Long-Term Income: Bonds are particularly appealing if you’re interested in generating a reliable stream of income over time. They offer regular interest payments throughout their term and promise the return of the principal amount upon maturity. However, it’s crucial to conduct thorough due diligence on the issuer’s financial health, especially with corporate bonds, to reduce the risk of default.

Where Can I Buy Bonds?

You can purchase bonds through brokerages, bond mutual funds, or, in the case of savings bonds, directly from the U.S. Treasury Department.

Please enable JavaScript in your browser to complete this form.

Bonds vs. CDs: How Do They Work?

Let’s break down the inner workings of both CDs and bonds. While they’re both commonly classified as safer investment options, the way they function and serve investors can be quite different.

How CDs Work

A Certificate of Deposit (CD) operates much like a time-specific savings account. When you open a CD, you deposit a fixed amount of money with a financial institution, like a bank or a credit union, for a fixed period. This period, often referred to as the term, can range from a few months to several years.

The bank will pay you interest on the money you’ve deposited. The interest rate is typically fixed, meaning it won’t change for the duration of the term. So, you’ll know exactly how much your CD will earn over its lifespan.

At the end of the term, the CD matures. You’ll receive the money you originally deposited plus the interest you’ve earned. If you withdraw your money before the end of the term, you’ll likely have to pay an early withdrawal penalty, which can eat into your earnings.

CDs are insured up to $250,000 per depositor by the Federal Deposit Insurance Corporation (FDIC) or the National Credit Union Administration (NCUA) if they’re offered by credit unions. This means even if the bank or credit union fails, your investment is secured.

How Bonds Work

Bonds operate more like loans — but you’re the lender. When you purchase a bond, you’re lending money to the issuer of the bond. This issuer could be a corporation, municipality, or the federal government. In return for the loan, the issuer promises to pay you a specified rate of interest during the life of the bond and to repay the face value of the bond (the principal) when it matures, or comes due.

The interest payment (also called the coupon payment) is usually paid semiannually. The rate is either fixed, meaning it won’t change for the life of the bond, or variable, adjusting with market conditions.

Bonds’ safety varies depending on the issuer. U.S. Treasury bonds, backed by the full faith and credit of the U.S. government, are considered the safest. Corporate bonds have different degrees of risk hinging on the financial health of the company. Municipal bonds’ safety depends on the financial health of the issuing local government. In general, the higher the risk, the higher the interest rate the bond will pay to compensate investors for taking on the additional risk.

Unlike CDs, bonds can be bought and sold on the secondary market before they mature. This provides liquidity but also introduces price risk. If you need to sell a bond before it matures, its price will depend on the current interest rate environment and the issuer’s creditworthiness. If interest rates have risen since you bought the bond, its value will have fallen, and you’ll get less than what you paid if you sell.

To summarize, while both CDs and bonds are tools for generating income, they function differently. CDs are time deposits with banks or credit unions, offering fixed, insured returns, ideal for short-to-medium-term financial goals. Bonds are essentially loans to corporations, municipalities, or the government. They offer variable returns (usually higher than CDs) and carry different levels of risk, which makes them suitable for a wider range of investment strategies and timelines.

What is the Difference Between CD and Bond? A Detailed Comparison

Safety

CDs and bonds are considered relatively safe. CDs, being insured by the FDIC or NCUA, offer a guaranteed return on your principal up to the insured amount. Bonds’ safety, on the other hand, depends on the issuer’s creditworthiness. Government-issued bonds are generally considered safer than corporate bonds.

Minimum Investment Requirements

Bonds often require higher minimum investments than CDs, sometimes going into the thousands of dollars. CDs, however, can be opened with a few hundred dollars, making them more accessible to investors with less capital.

Liquidity

Bonds generally offer more liquidity than CDs. If you need to cash in your investment, you can sell bonds before their maturity date without a penalty. Nevertheless, you may get less than the face value if bond prices have fallen. Contrariwise, CDs impose an early withdrawal penalty, making them less liquid.

Issuers and Protection

CDs are issued by banks and credit unions and are insured by the FDIC or NCUA. This insurance protects your investment even if the institution fails. For bonds, the mechanics are quite different: they are issued by corporations, municipalities, and the federal government. The safety of your bond investment primarily depends on the creditworthiness of the issuer.

Returns

Bonds often provide higher returns than CDs, depending on the type of bond and the issuer’s creditworthiness. This potential for higher returns comes with an increased risk. CDs offer a fixed interest rate and lower risk but often yield lower returns.

Penalties

If you withdraw money from a CD before its maturity date, you’ll incur an early withdrawal penalty. This can eat into your earned interest and sometimes even your principal. Bonds do not have early withdrawal penalties, but if you sell a bond before its maturity date, its value might be less than your original investment if bond prices have fallen.

Risks

While both CDs and bonds are considered low-risk investments, they have their unique risks. CDs come with reinvestment risk, which is the risk that when your CD matures, you may have to reinvest your money at a lower interest rate. Bonds, on the other hand, carry interest rate risk, which means that if interest rates rise, bond prices will fall, and vice versa.

The “Laddering” Approach for Investing in Bonds and CDs

Understanding how to manage your investment in bonds and CDs can make a significant difference in your return and overall experience. In my expertise, one of the most effective strategies is the “Laddering” approach.

When deciding between CDs vs bonds, the strategy of laddering could be an effective way to balance the liquidity and interest rate risks of both these fixed-income investments.

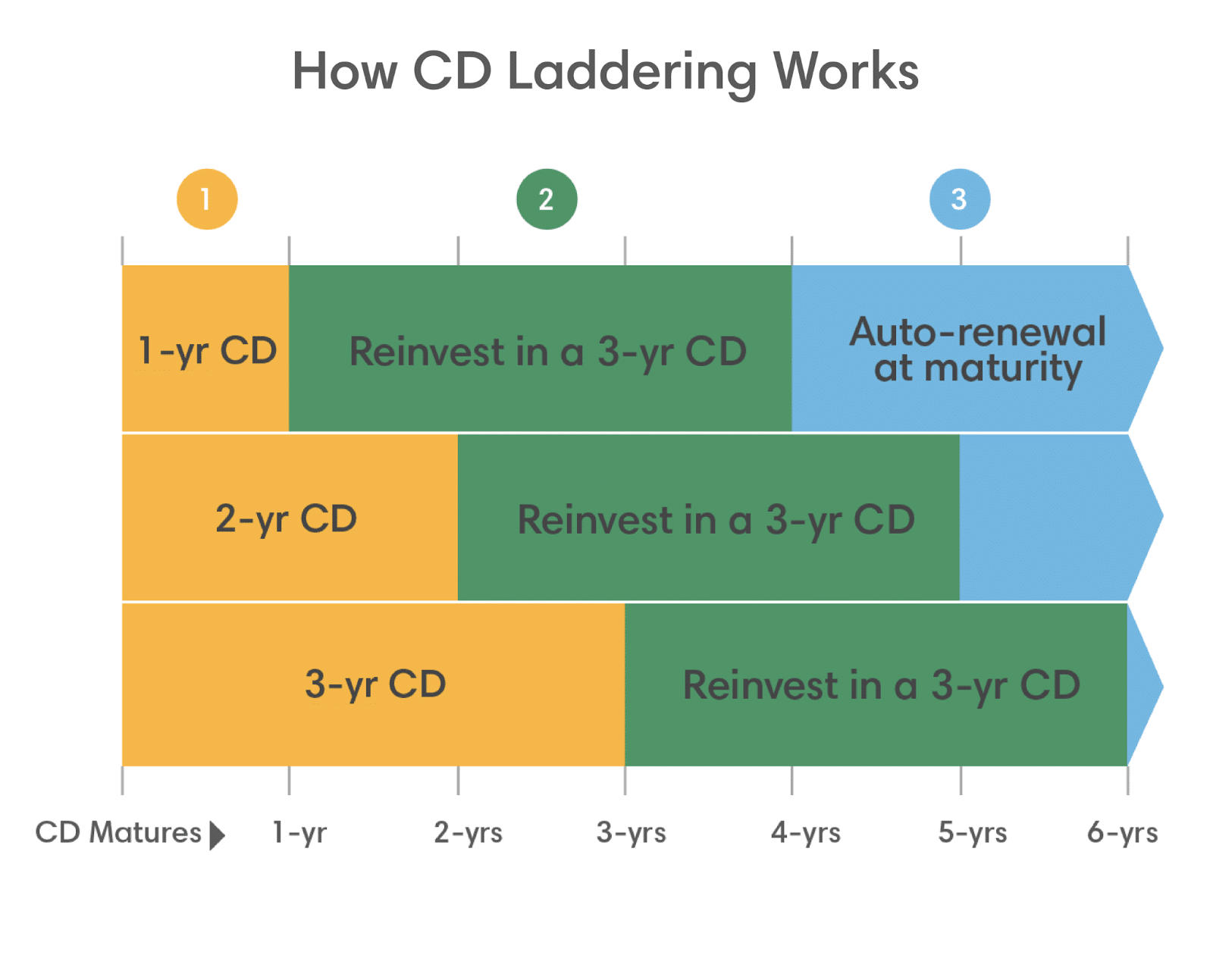

Let’s first clarify what exactly laddering is. When you “ladder” your CDs or bonds, you’re essentially diversifying your investments across different maturity dates. Imagine this strategy as a ladder where each rung represents a different maturity date, and the height corresponds to the length of the investment term.

For instance, instead of investing $15,000 into a single five-year CD, you could spread the investment across five CDs, each maturing one year apart. So, you might purchase five CDs worth $3,000 each with terms of one, two, three, four, and five years. This is your ladder.

Now let’s move on to why I consider this a strong strategy. Firstly, laddering reduces the impact of interest rate fluctuations. If all of your money is tied up in one long-term CD or bond, and interest rates rise, you miss out on these higher rates. However, with a laddered portfolio, some of your investments mature earlier, allowing you to take advantage of rising interest rates by reinvesting at these higher rates.

Secondly, laddering can provide a level of liquidity that one typically doesn’t associate with CDs and bonds. As each “rung” of your ladder matures, you have the option to access your money if needed, without incurring early withdrawal penalties that would typically be associated with accessing a single long-term CD or bond prematurely.

Using my knowledge, I would suggest laddering for those who want to invest in CDs or bonds but also want to mitigate interest rate risk and maintain some liquidity. This approach creates a balance between enjoying the higher rates offered by long-term investments and the flexibility of short-term ones.

In conclusion, based on my expertise in the field, I would recommend the laddering approach as a balanced, strategic method of investing in CDs and bonds. This approach allows you to capture high interest rates, provides regular access to funds without penalties, and reduces the risk of locking your whole investment at low rates. Still, as with all investment strategies, it’s essential to consider your financial situation, risk tolerance, and investment goals.

Although both are considered safer investments, the key difference in a CD vs a treasury bond discussion lies in liquidity — CDs typically incur penalties for early withdrawal, while treasury bonds can be sold on the secondary market. A CD still could be a better choice than a treasury bond if you prefer to invest with a bank or credit union and value the FDIC or NCUA insurance.

Bond vs. CD: FAQs

Can you lose money investing in CDs?

In theory, you cannot lose your principal in a CD as it is insured by the FDIC or NCUA. However, an early withdrawal penalty could reduce your overall return and, in some cases, eat into your principal.

Why do small investors prefer CDs?

Small investors favor Certificates of Deposit (CDs) due to their safety and predictability.

Insured up to $250,000 by federally insured banks or credit unions, CDs offer a risk-free investment alternative. They provide fixed interest rates over predetermined periods, ensuring stable, predictable returns unaffected by stock market volatility. This makes CDs attractive to those with specific savings goals or seeking portfolio diversification.

Furthermore, the current financial climate has seen high-yield CDs offering rates over 5%, some of the highest in over a decade, prompted by Federal Reserve rate hikes. This combination of security, predictability, and attractive returns positions CDs as a preferred option for small investors looking for low-risk investment avenues.

Are CDs safe if the market crashes?

Yes, CDs are considered safe investments, even during a market crash, because they are insured. This insurance means your investment is protected if the bank fails.

Which are the best bonds to buy now?

The best bonds to buy depend on your investment goals and risk tolerance. Government bonds are very safe but offer lower returns. Corporate bonds offer higher potential returns but carry more risk. Diversifying your bond investments, like investing in bond mutual funds, could be a good strategy to balance risk and reward.

Are bonds better than savings accounts?

Bonds and savings accounts serve different financial needs and goals. Bonds are generally considered a better option for long-term investments because they can offer higher returns over time compared to the interest rates typically offered by savings accounts. With bonds, you’re essentially lending money to an entity (like the government or a corporation) for a fixed period, during which you’ll receive interest payments. This mechanism can make bonds more attractive to those looking to grow their investment over several years.

However, savings accounts offer more liquidity, allowing for easier access to funds, which might be preferable for short-term savings or emergency funds. Each has its advantages depending on your investment horizon and need for access to your money.

Are bonds more liquid than CDs?

Yes, bonds are generally more liquid than CDs. You can sell bonds before their maturity date on the secondary market without incurring a penalty. On the other hand, if you withdraw money from a CD before its maturity date, you’ll face an early withdrawal penalty. It’s worth keeping in mind, though, that the amount you get for your bond might be less than its face value if bond prices have fallen.

Are bonds or CDs riskier?

While both are considered relatively low-risk investments, bonds can be riskier than CDs. The risk associated with bonds largely depends on the creditworthiness of the issuer. For instance, corporate bonds can carry a risk of default. CDs, however, are insured by the FDIC or NCUA, guaranteeing the return of your principal up to the insured amount, making them less risky.

Is a CD an asset?

Yes, a CD is considered an asset. When you purchase a CD, you are essentially lending money to a bank or a credit union for a set period, and in return, you receive a guaranteed amount of interest. This investment, including both the original deposit and the earned interest, is part of your financial assets.

The Bottom Line

CDs and bonds offer valuable ways to diversify your investment portfolio. CDs are better suited for risk-averse investors who want a guaranteed return and don’t need immediate access to their funds. Bonds can offer higher potential returns; they are suited for investors looking for regular income and the flexibility to sell before maturity.

Before investing, remember to pay attention to prevailing and expected future interest rates. If rates are expected to rise, short-term bonds or CDs may be beneficial as they would allow you to reinvest at higher rates sooner. If rates are predicted to fall, longer-term CDs or bonds may be more attractive — they would enable you to lock in a higher rate for a longer period.

Most importantly, understand your risk tolerance and financial goals before investing, and consider seeking advice from a financial advisor if you’re unsure. Happy investing!

References

- https://www.bankrate.com/banking/cds/how-do-cds-work/

- https://investor.vanguard.com/investor-resources-education/understanding-investment-types/what-is-a-bond

- https://www.dbs.com.sg/personal/investments/fixed-income/understanding-bonds#

- https://www.investor.gov/introduction-investing/investing-basics/investment-products/certificates-deposit-cds

- https://mint.intuit.com/blog/investments/money-market-vs-cd/

- https://www.fool.com/investing/how-to-invest/bonds/

Disclaimer: Please note that the contents of this article are not financial or investing advice. The information provided in this article is the author’s opinion only and should not be considered as offering trading or investing recommendations. We do not make any warranties about the completeness, reliability and accuracy of this information. The cryptocurrency market suffers from high volatility and occasional arbitrary movements. Any investor, trader, or regular crypto users should research multiple viewpoints and be familiar with all local regulations before committing to an investment.

The post CDs vs. Bonds: Which Is a Better Investment? A Comprehensive Guide appeared first on Cryptocurrency News & Trading Tips – Crypto Blog by Changelly.

#CDs #Bonds #Investment #Comprehensive #Guide